What Happens if You Are Covered With Blue Cross Blue Shield Insurance in Georgia January 2018

How much could you save on 2022 coverage?

Compare health insurance plans in New Mexico and check your subsidy savings.

Image: mojo_cp / stock.adobe.com

New Mexico health insurance marketplace 2022 guide

New state-run platform – bewellNM – replaces HealthCare.gov for enrollment in 2022 plans

- Louise Norris

- Health insurance & health reform authority

- April 28, 2022

New Mexico exchange overview

New Mexico uses a fully state-run health insurance exchange – beWellnm (also referred to as NMHIX, or the New Mexico Health Insurance Exchange). Six insurers offer exchange plans in New Mexico, although one of them — True Health — will exit the market at the end of 2022. During open enrollment for 2022 coverage, 45,664 people enrolled in private individual market plans through the New Mexico exchange.

Frequently asked questions about New Mexico's ACA marketplace

New Mexico has a state-run exchange, beWellnm (also referred to as NMHIX, or the New Mexico Health Insurance Exchange). For coverage effective in 2021 and previous years, the state used the federal enrollment platform at HealthCare.gov for individual enrollments. But as of November 2021 (for enrollment in 2022 coverage), New Mexico is running its own exchange platform and is no longer using HealthCare.gov.

New Mexico had initially planned to make this transition by the fall of 2020, but the board voted in 2019 to push the transition date out to the fall of 2021. For small businesses, New Mexico has long had its own SHOP exchange enrollment platform.

New Mexico previously had a unique exchange; the state ran the small-business portion, and while the individual exchange was also technically state-run, HealthCare.gov was used to enroll people in individual insurance (ie, a federally supported state-based exchange, or SBE-FP). But as of November 2021, the state fully runs both the small business and individual/family enrollment platforms.

Nevada transitioned back to having its own exchange platform as of the fall of 2019. Pennsylvania and New Jersey did so in the fall of 2020. Kentucky and Maine also transitioned to their own fully state-run exchanges in the fall of 2021, along with New Mexico. Virginia and Oregon are in varying stages of a future transition to fully state-run exchanges as well.

For 2022 coverage, there are six insurers that offer exchange plans in New Mexico:

- Blue Cross Blue Shield of New Mexico (Health Care Service Corporation)

- Friday Health Plans

- Molina

- Presbyterian Health Plan (rejoined the marketplace as of 2022)

- True Health (owned by Bright Health)

- Western Sky Community Care (Ambetter/Centene)

But in April 2022, Bright Health announced that they are exiting the markets in six states at the end of 2022, including New Mexico (where their plans are marketed as True Health, after Bright acquired True Health in 2021).

The New Mexico Office of the Superintendent of Insurance has published some helpful information for True Health members. All True Health individual market plans will end on December 31, 2022.

People who have individual/family True Health coverage through beWellnm will be automatically transitioned to a similar plan from another insurer as of January 2023, unless they actively select their own new plan during open enrollment. Actively selecting a new plan is the recommended approach.

People who purchased individual/family coverage directly from True Health (ie, off-exchange) will be uninsured as of January 2023 if they don't select a new plan. They can select a new plan off-exchange from a different insurer, or through beWellnm (subsidies are only available for plans selected through beWellnm).

Open enrollment for 2023 coverage begins November 1, 2022, but plans will be available for window shopping on beWellnm as of October 2022.

Insurer participation in New Mexico's exchange has been much more consistent over the years than insurer participation in other states. There are six insurers offering plans for 2022, but that's expected to drop to five in 2023, with True Health's exit from the market.

There were four insurers offering plans statewide in New Mexico every year except 2015 and 2021, when there were five. But there has been some musical chairs in terms of which insurers offered plans each year.

The Santa Fe New Mexican reported that there were only two health insurance companies offering individual coverage in New Mexico pre-ACA, so competition has increased in the state under the ACA. John Franchini, New Mexico's former Superintendent of Insurance, explained in 2016 that in terms of access to coverage and plan choice, New Mexico "in a much better place than we were four years ago. It's getting better and better." And insurer participation has grown even more since then.

In 2014, plans were available in the New Mexico exchange from Blue Cross Blue Shield of New Mexico (Health Care Service Corporation), Molina Healthcare of New Mexico, New Mexico Health Connections (one of the few ACA-created CO-OPs still operational as of 2020, but NM Health Connections closed at the end of 2020), and Presbyterian Health Plan.

In 2015, Christus Health Plan joined the exchange, and the four existing insurers continued to offer plans. The five insurers offered a total of more than 40 plans through the New Mexico exchange in 2015.

But for 2016, the New Mexico exchange dropped back down to four insurers after Blue Cross Blue Shield of New Mexico opted to leave the exchange at the end of 2015. In the summer of 2015, Blue Cross and Blue Shield of New Mexico filed a proposal to increase premiums for 2016 by an average of 51.6%. The announcement generated headlines nationwide, standing out even among some of the relatively steep rate increases proposed in other states. BCBS had about a third of the market share in the New Mexico exchange in 2015, so their proposed rate increase would have had a significant impact on the market.

But the New Mexico Office of the Superintendent of Insurance (OSI) denied the proposed rate hike, stating that the data submitted with the rate proposal didn't justify a rate increase of more than 24%. BCBS rejected the rate change offered by the state, but came back in the following days and submitted new rates that they claimed had an average rate increase of 11.3%. But the OSI has said that they didn't consider the secondary proposal to be a "real offer or realistic offer" and it was not accepted.

BCBSNM confirmed in late August that they would not be offering individual plans in the New Mexico exchange in 2016. They continued to offer one individual off-exchange plan — a bronze level HMO — with rates unchanged from 2015. This avoided a full market exit, meaning that BCBS preserved their option to return to the individual market with additional plans in 2017, which they decided to do (long-standing HIPAA rules prevent an insurer from returning to a market for five years after a full market exit).

So for 2016, plans were available in the New Mexico exchange from Christus, Molina, Presbyterian, and NM Health Connections. Individual market PPOs disappeared from the New Mexico exchange in 2016 (HMOs and EPOs help insurers control costs, so they've been steadily replacing PPOs in many markets).

Insurer participation changed again in 2017, but the total number of exchange insurers remained at four. Presbyterian Health Plan announced in July 2016 that they would transition to only offering off-exchange coverage in 2017. They noted that their on-exchange enrollees were incurring 30% more claims than their off-exchange enrollees, and Presbyterian determined that their on-exchange business was not sustainable. Through 2021, Presbyterian only offered off-exchange plans, although they returned to the exchange in 2022.

Blue Cross Blue Shield of New Mexico returned to the exchange for 2017. BCBSNM requested an average rate increase of 83.1% for their HMO product, but later revised it to 93.25 and regulators approved the requested rate hike. BCBSNM did not raise the rates on their remaining off-exchange HMO product for 2016, so the 93.2% rate increase was in relation to the 2015 rates.

For 2018 and 2019, there were no changes. Covered continues to be available from BCBSNM, Christus, Molina, and NM Health Connections. Presbyterian initially filed rates and plans to once again participate in the exchange starting in 2019, but ended up withdrawing that filing, noting that "due to concerns with current market environment, PHP has decided to continue offering plans only off the exchange." So Presbyterian's plans continued to be available only outside the exchange in 2019, and they didn't return to the exchange until 2022.

And although Molina threatened to exit New Mexico altogether at the end of 2018 when their Medicaid managed care contract was not renewed, that did not come to pass. An updated Molina rate filing, submitted in mid-August 2018, indicated that Molina was still planning to participate in the exchange in 2019, despite the fact that they still had a pending challenge to the Medicaid bidding process at that point. Molina's plans continue to be available in the New Mexico exchange in 2022, just as they have since 2014.

There were four insurers in New Mexico's exchange in 2020. but there were some changes: Christus, which had offered plans in the New Mexico exchange since 2015, failed to meet New Mexico's QHP certification requirements, so its plans had to terminate at the end of 2019. Christus covered about 1,100 people in New Mexico's individual market in 2019, all of whom needed to select new plans for 2020.

But True Health obtained individual market certification in New Mexico and offered coverage in the exchange as of 2020 — so New Mexico continued to have four exchange insurers. It's noteworthy that True Health was created in order to take over New Mexico Health Connection's employer-sponsored plans as of 2018 and allow NMHC to focus on the individual market. But as of 2020, both True Health and NMHC were offering individual market plans in the New Mexico exchange, in direct competition with each other.

Evolent paid $10.25 million to acquire NMHC's commercial insurance membership, and True Health New Mexico established an administrative services agreement that allowed them to support NMHC's ongoing operations in the individual market, while letting NMHC continue to be an independent non-profit. The administrative services relationship ended, however, at the end of 2019. For 2020, NMHC partnered with Friday Health Plans Management Services for plan administration. And in early 2021, True Health was acquired by Bright Health (more on that below; Bright Health is exiting six states at the end of 2022, including New Mexico).

New Mexico Health Connections closed its doors at the end of 2020 (leaving just three CO-OPs remaining nationwide, with plans available in five states).

But Friday Health Plans and Western Sky Community Care (Centene/Ambetter) joined New Mexico's exchange for 2021, bringing the total number of participating insurers to five. All marketplace insurers in New Mexico are required to offer plans statewide, so residents throughout New Mexico can choose from among all five insurers in 2021 (it's quite rare for all plan available in a state's marketplace to be available statewide, but New Mexico requires this, making the marketplace more robust, even in rural areas, than many other states' marketplaces).

For 2022, Presbyterian Health Plan rejoined the exchange, bringing the total number of participating insurers to six.

For 2023, however, True Health/Bright Health is exiting the market in New Mexico (Bright is exiting a total of five states at the end of 2022). If the other insurers all remain, New Mexico's exchange will once again have five insurers offering plans in 2023.

The open enrollment period for 2022 coverage ran from November 1, 2021 to January 15, 2022. The open enrollment period for 2023 coverage will run from November 1, 2022, through January 15, 2023.

Outside of the annual open enrollment window, you'll need a special enrollment period to enroll or make a change to your coverage. Most special enrollment periods are tied to a qualifying life event, although some special enrollment periods (such as the enrollment opportunity for Native Americans) do not require a specific life event.

If you have questions about enrollment opportunities, you can read more in our comprehensives guides to open enrollment and special enrollment periods.

New Mexico required insurers to price 2022 Silver plans in a manner that reflects their higher value based on integrated cost-sharing reductions that apply to most people who purchase Silver-level coverage.

Specifically, the state instructed insurers that they should assume that consumers will be rational and thus not purchase on-exchange Silver plans if their household income is above 200% of the poverty level (here's more about the reasoning for that). Below that income level, all Silver plans have actuarial values of 87% of 94%, which is well above the actuarial value of Gold plans. So the state instructed insurers to price Silver plans accordingly.

When Silver plan prices increase, premium subsidies increase too. Especially when you consider the more generous subsidy structure created by the American Rescue Plan, and the elimination of the income cap for subsidy eligibility in 2022, it's clear that coverage is much more affordable in New Mexico in 2022 for most consumers.

The NM Office of the Superintendent of Insurance published examples, illustrating just how much net premiums would decrease for enrollees who purchase 2022 coverage through New Mexico's exchange.

The following average rate changes were approved for 2022 in New Mexico. But again, it's important to understand that Silver plan rates increased more than other metal levels, which pushes subsidies higher and makes coverage more affordable for more people:

- Molina: Average increase of 25.7% (SERFF filing number MHNM-132884113). Molina had 11,667 members in 2021.

- Blue Cross Blue Shield of New Mexico (Health Care Service Corporation): Average decrease of 4.5% (SERFF filing number NWMC-132875074). BCBSNM/HCSC had 5,132 members.

- True Health: Average increase of 11.77% (SERFF filing number THNM-132869680). True Health had 14,881 members.

- Friday Health Plans: Average increase of 2.47%. (SERFF filing number COHP-132820405). Friday had 3,629 members.

- Western Sky Community Care (Ambetter/Centene): Average decrease of 4.17% (SERFF filing number CECO-132799464) Western Sky had 374 members.

- Presbyterian Health Plan: 0% rate change (SERFF filing PBHP-132855188) Presbyterian Health Plan has rejoined the exchange, after exiting at the end of 2016. Presbyterian had only offered off-exchange plans for the past five years, but resumed exchange participation for 2022. Presbyterian had 16,595 off-exchange enrollees in 2021.

Across all six insurers, the weighted average rate change amounts to an increase of about 8.6%. But that's before any subsidies are applied. Most enrollees qualify for subsidies (especially now that the American Rescue Plan is in place), and the subsidies are substantial for 2022. As the Office of the Superintendent of Insurance has clarified, most enrollees likely saw their net premiums decrease in 2022.

For perspective, here's a look back at how premiums have changed in previous years in New Mexico's marketplace:

2015: Average ratedecrease of 1.65%. The lowest-cost bronze plan in the NM exchange had averaged $217 a month in 2014, quite a bit lower than the national average of $249.

2016: Average rate increase of 4% (but BCBSNM enrollees had to switch plans). For 2016, BCBSNM did not offer plans in the exchange. Average rate changes for the other insurers ranged from a decrease of 2% for Molina to an increase of 4% to 17% for NM Health Connections. Overall, the average benchmark (second-lowest-cost Silver) plan in the New Mexico exchange was 7% more expensive in 2016 than in 2015 (an earlier HHS report pegged the increase at 25.8 percent, but that was because New Mexico Health Connections plans weren't appearing in the quote system due to the technical glitch, and their rates weren't taken into consideration when HHS initially analyzed the change in second-lowest-cost premium).

2017: Average rate increase of 28.4%. In 2017, with Presbyterian's exit and BCBSNM's return, four carriers offered 57 plans in the New Mexico exchange. Their approved average rate increases for 2017 were substantial, ranging from nearly 16% for Christus to more than 93% for BCBSNM. The average benchmark plan in New Mexico was 29% more expensive in 2017 than it was in 2016 (compared to an average of 22% across all 38 states that used HealthCare.gov in 2016). But to keep that data in context, we have to note that New Mexico's average benchmark premium was the lowest of all those 38 states in 2016, and even with the 29% average increase, New Mexico's benchmark premiums were still among the lowest-priced in 2017. They averaged $224/month for a 27-year-old, versus an average of $296/month across all the states that use HealthCare.gov.

2018: Average rate increase of about 30%. BCBSNM raised their average rates by about 26%, NM Health Connections by about 28%, Christus by about 49%, and Molina by more than 56%. New Mexico insurers were allowed to file two sets of rates, to accommodate the uncertainty that the Trump Administration created in the individual market — particularly the issue of whether federal funding would continue for the ACA's cost-sharing reductions (CSR). By September 2017, the insurers in New Mexico had all assumed that CSR funding would end, and had officially added the cost of CSR to silver plan premiums for 2018. The Trump administration ultimately did terminate CSR funding that October. The cost of CSR was added to premiums for silver exchange plans and the mirrored off-exchange versions of those silver plans, but silver off-exchange-only plans were also available without the cost of CSR added to their premiums.

The fact that the cost of CSR was added to silver plans resulted in larger premium subsidies for all subsidy-eligible enrollees in 2018, since subsidies are based on the cost of silver plans. Although the cost of CSR was added only to silver plan premiums, NMOSI also confirmed thatBlue Cross Blue Shield of New Mexico also added the cost of Native American cost-sharing reductions toall plans for 2018 (Native Americans can purchase $0 cost-sharing plans at all metal levels if their income doesn't exceed 300% of the poverty level). NMOSI noted that the cost of Native American CSR only added about 0.5% to 2% to the overall premiums for 2018, and the other three insurers didn't account for it in their rate filings. Essentially, BCBSNM was concerned that the potential elimination of CSR funding would include elimination of Native American CSR funding, so they added that cost to their 2018 premiums as well. CMS confirmed in November that all CSR funding had ended,including funding for the enhanced benefits for Native Americans. Although it's a much smaller total cost to insurers than regular CSR, insurers that didn't add the cost of Native American CSR to their 2018 premiums had to absorb the cost of enhanced benefits for Native Americans, while BCBSNM baked that cost into their premiums.

2019: Average ratedecrease of about 1%. On the heels of sharp rate increases in New Mexico's individual market for 2018, many consumers saw small ratedecreases for 2019. Insurers that offer on-exchange coverage were instructed by the New Mexico Office of the Superintendent of Insurance (NMOSI) to add the cost of cost-sharing reductions (CSR) only to on-exchange silver plans and the identical versions of those plans offered off-exchange (different silver plans offered only off-exchange do not have the cost of CSR added to their premiums).

In early 2018, Molina had threatened a possible exit of the individual market in New Mexico due to the impending loss of their Medicaid managed care contract. But Molina did file on- and off-exchange plans — with a proposed reduction in rates — and a revised filing, submitted in mid-August, indicated that they would continue to participate in the exchange, and with an even more significant rate reduction than they had originally proposed.

Off-exchange, Presbyterian Health Plan implemented an average rate increase of 18.5%. Presbyterian had 20,288 off-exchange members in 2018.

2020: Average rate increase of 0.9%. Although average rates increased only slightly for 2020 in New Mexico's individual market, it's important to note that average benchmark premiums in New Mexicodecreased by 6% for 2020. Premium subsidies — which 80% of New Mexico exchange enrollees receive — are based on the cost of the benchmark plan. So when benchmark rates decrease more sharply than overall average rates — which actually increased slightly in this case — the result can be an increase in net premiums for enrollees who receive subsidies. This essentially makes coverage less affordable than it was the year before, which could be a factor in New Mexico's lower enrollment for 2020.

There's an interesting note in the filing details for True Health: The insurer initially estimated that their risk adjustment receivables would amount to $19.24 per member per month, or about 4% of premiums. But they later revised that to 5.5%, which would have allowed them to reduce their proposed premiums. However, they submitted this modification to state regulators outside of the rate filing amendment period, so they were required to keep the estimated risk adjustment receivables at 4% of premiums.

This is what True Health explained in the filing notes:

"True Health is new to the individual market without any experience. The review was focused on actuarial assumptions and we requested support for these assumptions. The Company initially assumed a risk adjustment factor of 4.0%. The Company revised this assumption to 5.5% and this change was outside of the allowable amendment period. We requested additional support for the risk adjustment assumption. Ultimately, there was a conference call between Lewis & Ellis, True Health and the NM OSI. The Company provided adequate support for the 4.0% risk adjustment assumption. However, modifying this assumption outside of the amendment period was disallowed sine this would be an unfair advantage. The Company was required to revise the assumption back to the 4% of premium receivable."

But this is what the New Mexico Office of the Superintendent of Insurance explained:

"True Health is new to the individual market without any experience. The review was focused on assumptions like risk adjustment that required adequate support. The support provided continued to be inadequate in responses to inquiry and in fact, went further away from what would typically be expected as a new market entrant with low rates. Changes were made outside of the allowable amendment period. Ultimately, there was a conference call between Lewis & Ellis, True Health and the NM OSI to discuss. We were able to come to a reasonable conclusion that the Company had a reasonable rationale for the direction of the risk adjustment assumption (as a receivable). However, the conclusion was made that the Company did not provide enough support that they should be allowed an unfair advantage of revising the assumption after the amendment period, so the Company was required to revise the assumption back to the 4% of premium receivable."

Enrollment in New Mexico's exchange peaked in 2016, but declined by about 22% over the following four years. It increased slightly, however, for 2021, and grew significantly for 2022, reaching its highest level since 2018:

- 2014: 34,966 people enrolled

- 2015: 52,358 people enrolled

- 2016: 54,865 people enrolled

- 2017: 54,653 people enrolled

- 2018: 49,792 people enrolled

- 2019: 45,001 people enrolled

- 2020: 42,714 people enrolled

- 2021: 42,984 people enrolled

- 2022: 45,664 people enrolled

Across most of the states that use HealthCare.gov, enrollment tended to peak in 2016 and decline over the following four years, with a modest increase in enrollment coming in 2021 (and record-high enrolment in 2022). But most of the other state-based exchanges that use the federal HealthCare.gov enrollment platform (SBE-FPs), including Kentucky, Oregon, Virginia, and Maine, saw an enrollment drop in 2021. Arkansas and New Mexico were the only SBE-FPs that saw enrollment increase from 2020 to 2021. Nationwide, enrollment hit a new record high for 2022, driven in large part by the American Rescue Plan's subsidy enhancements.

Would ACA subsidies lower your health insurance premiums?

Use our 2022 subsidy calculator to see if you're eligible for ACA premium subsidies – and your potential savings if you qualify.

Obamacare subsidy calculator *

Estimated annual subsidy

Provide information above to get an estimate.

* This tool provides ACA premium subsidy estimates based on your household income. healthinsurance.org does not collect or store any personal information from individuals using our subsidy calculator.

New Mexico's multi-year process of becoming a fully state-run exchange

New Mexico's path to establishing an exchange was atypical. Then-Governor Susana Martinez, a Republican who opposed the federal health reform law, was the driving force in establishing an exchange and advocating for the state-run model.

Martinez designated that the Health Insurance Alliance to develop the state exchange. The Health Insurance Alliance is a nonprofit association of health plans created by the state Legislature in 1994 to offer health insurance coverage to small employers. Later, the Senate and House both approved a state-run exchange.

But New Mexico has always used HealthCare.gov's enrollment platform for individual market enrollments, so the exchange has been classified as a federally-supported state-based exchange. That changed in 2021, however, when New Mexico unveiled its own state-run enrollment platform and stopped using HealthCare.gov.

Initially, the state had planned to establish a state-run website for individual enrollments fairly soon after the exchanges went live in the fall of 2013, and that was still in the works until early spring 2015. But in April 2015, the exchange board voted to continue to use HealthCare.gov, as that was viewed as the less-costly alternative.

New Mexico's exchange had completed about 75 percent of its enrollment website when HHS changed the design guidelines in the fall of 2014. The exchange then applied for a $97 million federal grant to help pay for the website changes as well as other costs, but the grant was denied. Ultimately, it was decided in 2015 that continuing to use Healthcare.gov would be the most fiscally responsible option. And the state has continued to use the federal enrollment platform ever since.

But although the federal government initially didn't charge state-based exchanges for the use of HealthCare.gov, they began doing so as of 2017. In 2020 and 2021, state-based exchanges that use HealthCare.gov must pay a user fee equal to 2.5 percent of premiums (this is a reduction from the 3 percent that was charged in 2019).

In 2018, beWellnm (the state-run exchange) paid $5.4 million to the federal government for the use of the HealthCare.gov enrollment platform. For 2019, it was expected that the exchange would have to pay $10.9 million to use HealthCare.gov. In order to reduce user fees, the exchange board considered the issue during a September 2018 board meeting, and voted unanimously to transition to a fully state-run exchange in time for the 2021 plan year. In 2019, however, the exchange board voted to push the transition time frame out by one year, so beWellnm will be the official exchange platform starting in the fall of 2021 (instead of 2020), when people are purchasing coverage for 2022.

A presentation during the March 2019 board meeting indicated that New Mexico will begin to reap cost savings from switching to a state-run exchange by 2023 or 2024. There will be an initial spike in costs as the state pays for the creation of the new exchange, but costs will then decline sharply and flatten out. On the other hand, continuing to use HealthCare.gov would mean that the cost to use the exchange would climb as premiums increase over time, since it's based on a percentage of premiums.

H.B.100, enacted in early 2020, provides legislative guidance for the fully state-run exchange. It builds and expands on S.B.221, which was enacted in 2013 and established guidelines for the creation of New Mexico's exchange. H.B.100 adds various provisions, and grants additional authority to the exchange board, including the option to create standardized plan designs and establish appropriate enrollment periods (fully state-run exchanges can offer longer enrollment periods, whereas states that use HealthCare.gov do not have any flexibility in this area).

New Mexico replaces the ACA's health insurance tax; uses revenue to make coverage and care more affordable in state

The ACA's health insurance tax no longer applies after the end of 2020. So lawmakers in New Mexico considered legislation in 2020 (H.B.278) that would have replaced the federal tax with one levied by the state and use the revenue to make health coverage and health care more affordable for people who buy plans through New Mexico Health Connection. Although the legislation passed in the House in February 2020, it died in the Senate without getting a hearing.

Lawmakers were successful in 2021, however, with S.B.317, which creates the Health Care Affordability Fund in New Mexico, and also eliminates cost-sharing when people with state-regulated health plans (ie, plans that aren't self-insured) seek behavioral health care. (Note that H.B.122 had been introduced earlier in 2021 in an effort to reach the same goal, but the provisions were ultimately added to S.B.317 instead.)

Under S.B.317, New Mexico has added a new tax of roughly 2.75% of health insurance premiums, starting in 2022. This amount is very similar to the federal health insurance tax that applied until the end of 2020. The money generated by this additional tax will be directed to the Health Care Affordability Fund, administered by the New Mexico Office of the Superintendent of Insurance to "reduce health care premiums and cost-sharing for New Mexico residents who purchase health care coverage on the New Mexico health insurance exchange; provide resources for planning, design, and implementation of health care coverage initiatives for uninsured New Mexico residents; and provide resources for administration of state health care coverage initiatives for uninsured New Mexico residents."

The fee will generate an estimated $165 million in annual funding, which will be collected by the state rather than the federal government (until the end of 202o, insurers sent these fees to the federal government). The state will then use the money to reduce the cost of health care coverage for New Mexico residents, including measures such as state-funded premium subsidies and cost-sharing assistance.

Colorado enacted a similar bill in 2020, designed to extend funding for the state's existing reinsurance program and also provide additional state-based subsidies to make coverage and care more affordable.

California began offering state-based premium subsidies in 2020 (although they are no longer necessary as long as the American Rescue Plan's subsidy structure remains in place), and New Jersey began offering state-based subsidies in 2021. Washington has enacted legislation that creates a state-funded subsidy program as of 2023. Massachusetts and Vermont both also have state-funded subsidies for lower-income residents.

New Mexico lawmakers unanimously approve "easy enrollment" program legislation

In March 2021, New Mexico's House of Representatives passed H.B.272, which called for the state to create an "easy enrollment" program for health coverage. But the legislation subsequently died in the state Senate, and thus did not come to fruition in 2021.

However, similar legislation (H.B.95) was reintroduced in 2022, and unanimously passed both chambers of the New Mexico legislature. Assuming it's signed into law, it would create an easy enrollment program that would be in use as of early 2023, when 2022 tax returns are being filed.

Under this program, New Mexico state tax returns would allow residents who are uninsured to consent to have their relevant information shared with the state Medicaid office and the state-run health insurance exchange (beWellnm).

If the state determines that they're eligible for Medicaid, they would be automatically enrolled. If the preliminary determination is that the person would instead be eligible for a qualified health plan (ie, a private plan offered by the exchange), the exchange will send the person information about enrolling in a plan and will provide them with a special enrollment period during which they can do so. (The special enrollment period would be necessary because open enrollment for qualified health plans ends in mid-January, well before the tax-filing season. Without a special enrollment period, the person would have to wait until November to sign up for coverage.)

Several other states have already created easy enrollment programs, including Maryland, Colorado, Pennsylvania, and Massachusetts. Others are partially in place or still being considered by state legislatures and more are likely to debut in future years.

CO-OP closed at the end of 2020

New Mexico had four individual market insurers in 2020, but New Mexico Health Connections — one of just four remaining ACA-created CO-OPs in the nation — closed at the end of 2020 and did not offer plans for 2021. But two new insurers — Friday Health Plans and Western Sky Community Care (Ambetter/Centene) — joined New Mexico's marketplace for 2021.

It's noteworthy that SERFF filings indicated that in May 2020, New Mexico's Superintendent of Insurance contacted all of the insurers that offer ACA-compliant coverage in New Mexico, stating "I would like for you to give consideration to offering at least one plan that has a lower max out of pocket limit than the plans currently offered on the Exchange. While I thank all the current offerors for their very reasonably priced current offerings, the single most common complaint we receive is about the $6-8k max out of pocket caps. For many enrolled through the Exchange, these maximums are truly unaffordable. I am afraid they also discourage some individuals from enrolling for coverage." During the process of reviewing rates in 2020, insurance regulators were specifically asking insurers how they accounted for this request in their proposals for 2021.

For the three insurers that offered plans in 2020, the approved rates for 2021 were lower than the insurers had initially proposed, resulting in an overall average rate decrease of about 1.5% for 2021. New Mexico Health Connection's 14,000 members all had to transition to other plans for 2021.

New Mexico Health Connections had struggled financially over the years, but had weathered the early rounds of widespread CO-OP closures. The economic downturn caused by COVID-19 resulted in declining enrollment, with some of the CO-OP's members transitioning to Medicaid in 2020 after losing their income. The CO-OP had about 17,000 members as of late 2019, and that had dropped to about 14,000 by August 2020.

The New Mexico Office of the Superintendent of Insurance published a set of FAQs about the CO-OP closure. Notably, CO-OP members who had their coverage through the New Mexico exchange were automatically enrolled in a comparable plan from another insurer if they didn't select their own replacement plan during open enrollment.

New Mexico's surprise balance billing protection took effect in 2020

During the 2019 legislative session, New Mexico enacted SB337, which took effect in January 2020, protecting New Mexico residents (who have state-regulated health plans) from surprise balance billing.

Balance billing happens when a patient uses an out-of-network provider and the provider bills the patient for any portion of the charges that aren't covered by health insurance. The "surprise" part refers to situations in which the person either had no choice but to use an out-of-network provider (ie, an emergency), or situations in which the patient used an in-network facility but was — usually unbeknownst to the patient — treated by an ancillary provider at that facility who wasn't in the patient's insurance network (eg. anesthesiologists, radiologists, pathologists, assistant surgeons, etc.).

Under the state's new law, patients cannot be charged more than their regular in-network cost-sharing obligations (copays, deductible, coinsurance, up to the maximum out-of-pocket level for their plan) if they:

- receive emergency care at an out-of-network facility.

- receive non-emergency care from an out-of-network provider at an in-network facility, as long as the patient either had "no ability or opportunity" to receive the care from an in-network provider instead. This includes situations in which there is no in-network provider available.

The New Mexico Office of the Superintendent of Insurance has clarified all of this in a bulletin that was published in May 2019.

As is the case with any state-based rules, New Mexico's new law does not apply to self-insured plans in the state, which are regulated under federal law (ERISA) rather than state law. Most very large group plans are self-insured, but New Mexico's new rules apply to individual market plans in the state, as well as fully-insured (as opposed to self-insured) group plans. Fortunately for people with self-insured coverage, the federal No Surprises Act took effect in January 2022, providing nationwide, federally-regulated protections against surprise balance billing.

For 2018 plans, subsidies differed depending on when people enrolled

New Mexico's path to establishing an exchange was atypical. Then-Governor Susana Martinez, a Republican who opposed the federal health reform law, was the driving force in establishing an exchange and advocating for the state-run model.

Martinez designated that the Health Insurance Alliance to develop the state exchange. The Health Insurance Alliance is a nonprofit association of health plans created by the state Legislature in 1994 to offer health insurance coverage to small employers. Later, the Senate and House both approved a state-run exchange.

But New Mexico has always used HealthCare.gov's enrollment platform for individual market enrollments, so the exchange has been classified as a federally-supported state-based exchange. That will change in the fall of 2021, however, when New Mexico plans to unveil its own state-run enrollment platform and stop using HealthCare.gov.

New Mexico health insurance exchange links

Other types of health coverage in New Mexico

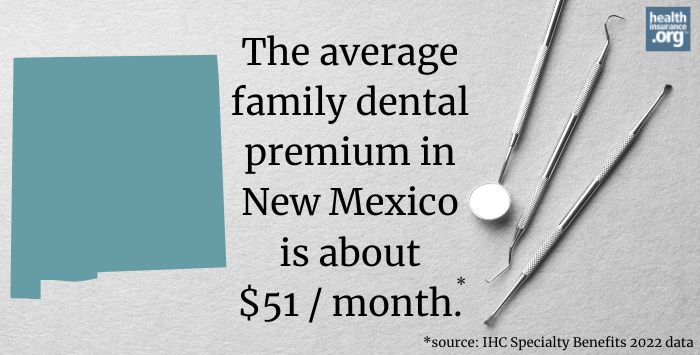

Dental Insurance in New Mexico

Learn about adult and pediatric dental insurance options in New Mexico, including stand-alone dental and coverage through BeWellNM, the state's health insurance marketplace.

Source: https://www.healthinsurance.org/health-insurance-marketplaces/new-mexico/

{kind=link}

Enviar um comentário for "What Happens if You Are Covered With Blue Cross Blue Shield Insurance in Georgia January 2018"